One of many extra silly arguments 1 that appear to be emanating from the Fed about their intention to boost charges one other quarter level immediately: The two% inflation goal that has been in place just about all the post-financial disaster period.

There isn’t any empirical proof exhibiting 2% is the optimum long-run inflation goal, given the Fed’s twin mandate of worth stability and most employment. It’s a kind of spherical numbers that individuals simply kinda made up and began with for no obvious motive.

If there was one thing magical about 2% as the perfect steadiness between costs and jobs, that may be one factor. However the 2% inflation goal is LITERALLY a random quantity 2 that originated in New Zealand within the 1980s. “Surprisingly, it got here not from any tutorial examine,” CFR observes, “however reasonably from an offhand remark throughout a tv interview.” For causes nobody has intelligently articulated, different international locations subsequently adopted it as their goal.

Laurence Ball, Professor of Economics at Johns Hopkins and Analysis Affiliate on the Nationwide Bureau Of Financial Analysis, made the case in 2013 that 4% was a extra rational goal. “Elevating inflation targets to 4% would have little price, and it might make it simpler for central banks to finish future recessions,” he famous.3

The Federal Open Market Committee has justified the two% inflation based mostly on inflation expectations. The Board of Governors acknowledged, “When households and companies can moderately count on inflation to stay low and secure, they’re able to make sound choices concerning saving, borrowing, and funding, which contributes to a well-functioning financial system.”

The issue with this method is as we now have repeatedly proven, it’s completely ineffective. Inflation expectations are sometimes at their lowest proper earlier than a surge in inflation happens; they’re at their highest ranges simply as inflation rolls over and heads downwards. Individuals’s inflation expectations mimic the everyday overenthusiastic investor, piling in on the prime of the market and panic promoting close to the underside.

Expectations aren’t any approach to run financial coverage and are healthier for a Monty Python movie.4

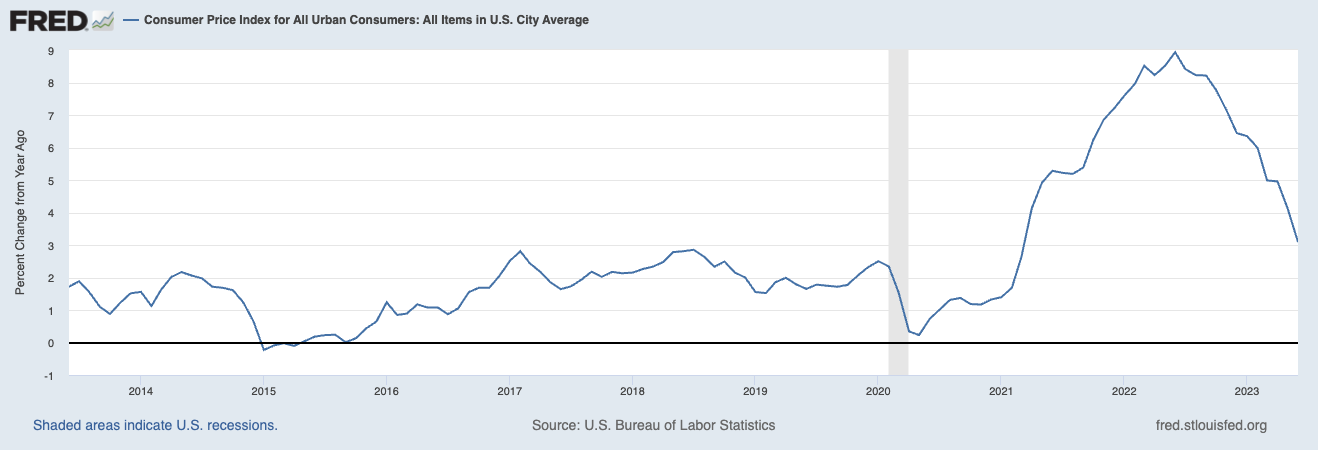

Take into account: We had 2% inflation expectations all the post-GFC period. The financial system was sluggish, job creation as weak, client spending was comfortable. ZIRP and QE had pushed charges to zero (or damaging in some components of the world), and a pair of% appeared an inexpensive albeit arbitrary upside goal. However after $6 trillion in fiscal stimulus, mortgage charges at 7.5%, maybe 3% makes rather more sense as a draw back inflation goal.

I’ve famous up to now that the Fed was late to get off its emergency footing, late to acknowledge inflation pierced its 2% goal to the upside (March 2021), late to start elevating charges (March 2022), late to acknowledge inflation had peaked (June 2022), late to acknowledge that they’ve already crushed inflation in (July 2023).

I’ve a pet concept as to why they’ve been constantly so late: Many economists have misunderstood this whole financial cycle, together with inflation. These older faculty economists – who demanded vigilance towards rising costs, declared inflation to be persistent, sticky, and non-transitory and even stagflationary – all made their bones within the 1970s/80s. They’re haunted by a really completely different sort of financial system that had very completely different inflation drivers. Their PTSD is palpable.

They’re taking the fallacious lesson from that period. As Professor Ball wryly noticed to the NYT’s Jeff Sommers, “If 4% was ok for Volcker, it ought to be ok for us.”

Beforehand:

A Dozen Contrarian Ideas About Inflation (July 13, 2023)

Extra Inflation Expectations Silliness (July 5, 2023)

Inflation Expectations Are Ineffective (Could 17, 2023)

For Decrease Inflation, Cease Elevating Charges (January 18, 2023)

Why Is the Fed At all times Late to the Celebration? (October 7, 2022)

Inflation Expectations: A Doubtful Survey (September 21, 2022)

Transitory Is Taking Longer than Anticipated (February 10, 2022)

__________

1. Let’s maintain apart the declare that the Fed must “preserve credibility,” as that squishy argument is just too ridiculous to handle.

2. The case for 4% inflation, Laurence Ball, VoxEU/CEPR 24 Could 2013

3. Like 20% for a bull or bear market, its made up, with none information supporting it as both an indicator or a predictor.

4. Peasants: We now have discovered a witch! (A witch! a witch!)

Burn her burn her!

Peasant 1: We now have discovered a witch, might we burn her?

(cheers)

Vladimir: How do you recognized she is a witch?

P2: She seems to be like one!

V: Carry her ahead

(advance)

Lady: I’m not a witch! I’m not a witch!

V: ehh… however you’re dressed like one.

W: They dressed me up like this!

All: naah no we didn’t… no.

W: And this isn’t my nostril, it’s a false one.

(V lifts up carrot)

V: Effectively?

P1: Effectively we did do the nostril

V: The nostril?

P1: …And the hat, however she is a witch!

(all: yeah, burn her burn her!)

V: Did you costume her up like this?

P1: No! (no no… no) Sure. (sure yeah) a bit (a bit bit a bit) However she has acquired a wart!

(P3 factors at wart)

V: What makes you suppose she is a witch?

P2: Effectively, she turned me right into a newt!

V: A newt?!

(P2 pause & go searching)

P2: I acquired higher.