This submit takes up from two earlier posts (half 1; half 2), asking simply what can we (we economists) actually find out about how rates of interest have an effect on inflation. At the moment, what does modern financial concept say?

As you might recall, the usual story says that the Fed raises rates of interest; inflation (and anticipated inflation) do not instantly bounce up, so actual rates of interest rise; with some lag, increased actual rates of interest push down employment and output (IS); with some extra lag, the softer economic system results in decrease costs and wages (Phillips curve). So increased rates of interest decrease future inflation, albeit with “lengthy and variable lags.”

Increased rates of interest -> (lag) decrease output, employment -> (lag) decrease inflation.

Partly 1, we noticed that it isn’t simple to see that story within the information. Partly 2, we noticed that half a century of formal empirical work additionally leaves that conclusion on very shaky floor.

As they are saying on the College of Chicago, “Effectively, a lot for the true world, how does it work in concept?” That is a crucial query. We by no means actually consider issues we do not have a concept for, and for good cause. So, at this time, let us take a look at what trendy concept has to say about this query. And they aren’t unrelated questions. Principle has been attempting to copy this story for many years.

The reply: Fashionable (something submit 1972) concept actually doesn’t assist this concept. The usual new-Keynesian mannequin doesn’t produce something like the usual story. Fashions that modify that easy mannequin to realize one thing like results of the usual story achieve this with an extended checklist of complicated components. The brand new components will not be simply adequate, they’re (apparently) obligatory to supply the specified dynamic sample. Even these fashions don’t implement the verbal logic above. If the sample that prime rates of interest decrease inflation over just a few years is true, it’s by a very completely different mechanism than the story tells.

I conclude that we do not have a easy financial mannequin that produces the usual perception. (“Easy” and “financial” are vital qualifiers.)

The easy new-Keynesian mannequin

The central downside comes from the Phillips curve. The fashionable Phillips curve asserts that price-setters are forward-looking. In the event that they know inflation will probably be excessive subsequent yr, they increase costs now. So

Inflation at this time = anticipated inflation subsequent yr + (coefficient) x output hole.

[pi_t = E_tpi_{t+1} + kappa x_t](If sufficient to complain about (betaapprox0.99) in entrance of (E_tpi_{t+1}) sufficient that it does not matter for the problems right here.)

Now, if the Fed raises rates of interest, and if (if) that lowers output or raises unemployment, inflation at this time goes down.

The difficulty is, that is not what we’re searching for. Inflation goes down at this time, ((pi_t))relative to anticipated inflation subsequent yr ((E_tpi_{t+1})). So a better rate of interest and decrease output correlate with inflation that’s rising over time.

Here’s a concrete instance:

The plot is the response of the usual three equation new-Keynesian mannequin to an (varepsilon_1) shock at time 1:[begin{align} x_t &= E_t x_{t+1} – sigma(i_t – E_tpi_{t+1}) pi_t & = beta E_t pi_{t+1} + kappa x_t i_t &= phi pi_t + u_t u_t &= eta u_{t-1} + varepsilon_t. end{align}] Right here (x) is output, (i) is the rate of interest, (pi) is inflation, (eta=0.6), (sigma=1), (kappa=0.25), (beta=0.95), (phi=1.2).

On this plot, increased rates of interest are mentioned to decrease inflation. However they decrease inflation instantly, on the day of the rate of interest shock. Then, as defined above, inflation rises over time.

In the usual view, and the empirical estimates from the final submit, a better rate of interest has no rapid impact, after which future inflation is decrease. See plots within the final submit, or this one from Romer and Romer’s 2023 abstract:

Inflation leaping down after which rising sooner or later is sort of completely different from inflation that does nothing instantly, would possibly even rise for just a few months, after which begins gently taking place.

You would possibly even surprise concerning the downward bounce in inflation. The Phillips curve makes it clear why present inflation is decrease than anticipated future inflation, however why does not present inflation keep the identical, and even rise, and anticipated future inflation rise extra? That is the “equilibrium choice” challenge. All these paths are potential, and also you want further guidelines to choose a selected one. Fiscal concept factors out that the downward bounce wants a fiscal tightening, so represents a joint monetary-fiscal coverage. However we do not argue about that at this time. Take the usual new Keynesian mannequin precisely as is, with passive fiscal coverage and customary equilibrium choice guidelines. It predicts that inflation jumps down instantly after which rises over time. It doesn’t predict that inflation slowly declines over time.

This isn’t a brand new challenge. Larry Ball (1994) first identified that the usual new Keynesian Phillips curve says that inflation is excessive when inflation is excessive relative to anticipated future inflation, that’s when inflation is declining. Normal beliefs go the opposite method: output is excessive when inflation is rising.

The IS curve is a key a part of the general prediction, and output faces an analogous downside. I simply assumed above that output falls when rates of interest rise. Within the mannequin it does; output follows a path with the identical form as inflation in my little plot. Output additionally jumps down after which rises over time. Right here too, the (a lot stronger) empirical proof says that an rate of interest rise doesn’t change output instantly, and output then falls moderately than rises over time. The instinct has even clearer economics behind it: Increased actual rates of interest induce folks to eat much less at this time and extra tomorrow. Increased actual rates of interest ought to go together with increased, not decrease, future consumption development. Once more, the mannequin solely apparently reverses the signal by having output bounce down earlier than rising.

Key points

How can we be right here, 40 years later, and the benchmark textbook mannequin so totally doesn’t replicate customary beliefs about financial coverage?

One reply, I consider, is complicated adjustment to equilibrium with equilibrium dynamics. The mannequin generates inflation decrease than yesterday (time Zero to time 1) and decrease than it in any other case can be (time 1 with out shock vs time 1 with shock). Now, all financial fashions are a bit stylized. It is simple to say that once we add varied frictions, “decrease than yesterday” or “decrease than it will have been” is an efficient parable for “goes down over time.” If in a easy provide and demand graph we are saying that a rise in demand raises costs immediately, we naturally perceive that as a parable for a drawn out interval of value will increase as soon as we add acceptable frictions.

However dynamic macroeconomics does not work that method. We now have already added what was imagined to be the central friction, sticky costs. Dynamic economics is meant to explain the time-path of variables already, with no further parables. If adjustment to equilibrium takes time, then mannequin that.

The IS and Phillips curve are ahead wanting, like inventory costs. It might make little sense to say “information comes out that the corporate won’t ever earn cash, so the inventory value ought to decline steadily over just a few years.” It ought to bounce down now. Inflation and output behave that method in the usual mannequin.

A second confusion, I feel, is between sticky costs and sticky inflation. The brand new-Keynesian mannequin posits, and an enormous empirical literature examines, sticky costs. However that isn’t the identical factor as sticky inflation. Costs will be arbitrarily sticky and inflation, the primary by-product of costs, can nonetheless bounce. Within the Calvo mannequin, think about that solely a tiny fraction of corporations can change costs at every prompt. However after they do, they’ll change costs quite a bit, and the general value degree will begin growing immediately. Within the continuous-time model of the mannequin, costs are steady (sticky), however inflation jumps in the intervening time of the shock.

The usual story needs sticky inflation. Many authors clarify the new-Keynesian mannequin with sentences like “the Fed raises rates of interest. Costs are sticky, so inflation cannot go up immediately and actual rates of interest are increased.” That is fallacious. Inflation can rise immediately. In the usual new-Keynesian mannequin it does so with (eta=1), for any quantity of value stickiness. Inflation rises instantly with a persistent financial coverage shock.

Simply get it out of your heads. The usual mannequin doesn’t produce the usual story.

The plain response is, let’s add components to the usual mannequin and see if we will modify the response perform to look one thing just like the widespread beliefs and VAR estimates. Let’s go.

Adaptive expectations

We will reproduce customary beliefs about financial coverage with completely adaptive expectations, within the 1970s ISLM kind. I feel it is a giant a part of what most coverage makers and commenters keep in mind.

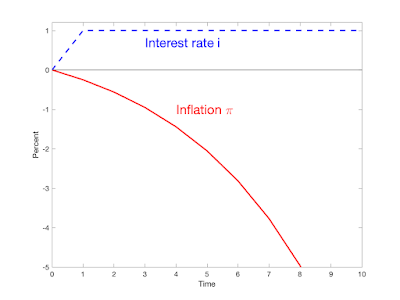

Modify the above mannequin to go away out the dynamic a part of the intertemporal substitution equation, to simply say in moderately advert hoc method that increased actual rates of interest decrease output, and specify that the anticipated inflation that drives the true price and that drives pricing selections is mechanically equal to earlier inflation, (E_t pi_{t+1} = pi_{t-1}). We get [ begin{align} x_t &= -sigma (i_t – pi_{t-1}) pi_t & = pi_{t-1} + kappa x_t .end{align}] We will resolve this sytsem analytically to [pi_t = (1+sigmakappa)pi_{t-1} + sigmakappa i_t.]

Here is what occurs if the Fed completely raises the rate of interest. Increased rates of interest ship future inflation down. ((kappa=0.25, sigma=1.)) Inflation ultimately spirals away, however central banks do not go away rates of interest alone ceaselessly. If we add a Taylor rule response (i_t = phi pi_t + u_t), so the central financial institution reacts to the rising spiral, we get this response to a everlasting financial coverage disturbance (u_t):

The upper rate of interest units off a deflation spiral. However the Fed rapidly follows inflation right down to stabilize the scenario. That is, I feel, the traditional story of the 1980s.

- Behavior formation. The utility perform is (log(c_t – bc_{t-1})).

- A capital inventory with adjustment prices in funding. Adjustment prices are proportional to funding development, ([1-S(i_t/i_{t-1})]i_t), moderately than the same old formulation wherein adjustment prices are proportional to the funding to capital ratio (S(i_t/k_t)i_t).

- Variable capital utilization. Capital companies (k_t) are associated to the capital inventory (bar{ok}t) by (k_t = u_t bar{ok}_t). The utilization price (u_t) is ready by households going through an upward sloping value (a(u_t)bar{ok}_t).

- Calvo pricing with indexation: Corporations randomly get to reset costs, however corporations that are not allowed to reset costs do routinely increase costs on the price of inflation.

- Costs are additionally mounted for 1 / 4. Technically, corporations should submit costs earlier than they see the interval’s shocks.

- Sticky wages, additionally with indexation. Households are monopoly suppliers of labor, and set wages Calvo-style like corporations. (Later papers put all households right into a union which does the wage setting.) Wages are additionally listed; Households that do not get to reoptimize their wage nonetheless increase wages following inflation.

- Corporations should borrow working capital to finance their wage invoice 1 / 4 prematurely, and thus pay a curiosity on the wage invoice.

- Cash within the utility perform, and cash provide management. Financial coverage is a change within the cash development price, not a pure rate of interest goal.

… the rate of interest seems in corporations’ marginal value. Because the rate of interest drops after an expansionary financial coverage shock, the mannequin embeds a pressure that pushes marginal prices down for a time frame. Certainly, within the estimated benchmark mannequin the impact is powerful sufficient to induce a transient fall in inflation.

That is about the place we’re. Regardless of the beautiful response features, I nonetheless rating that we do not have a dependable, easy, financial mannequin that produces the usual view of financial coverage.

Mankiw and Reis, sticky expectations

Mankiw and Reis (2002) expressed the problem clearly over 20 years in the past. In reference to the “customary” New-Keynesian Phillips curve (pi_t = beta E_t pi_{t+1} + kappa x_t) they write a ravishing and succinct paragraph:

Ball [1994a] reveals that the mannequin yields the shocking consequence that introduced, credible disinflations trigger booms moderately than recessions. Fuhrer and Moore [1995] argue that it can’t clarify why inflation is so persistent. Mankiw [2001] notes that it has bother explaining why shocks to financial coverage have a delayed and gradual impact on inflation. These issues seem to come up from the identical supply: though the value degree is sticky on this mannequin, the inflation price can change rapidly. In contrast, empirical analyses of the inflation course of (e.g., Gordon [1997]) sometimes give a big position to “inflation inertia.”

At the price of repetition, I emphasize the final sentence as a result of it’s so ignored. Sticky costs will not be sticky inflation. Ball already mentioned this in 1994:

Taylor (1979, 198) and Blanchard (1983, 1986) present that staggering produces inertia within the value degree: costs simply slowly to a fall in th cash provide. …Disinflation, nonetheless, is a change within the development price of cash not a one-time shock to the extent. In casual discussions, analysts typically assume that the inertia consequence carries over from ranges to development charges — that inflation adjusts slowly to a fall in cash development.

As I see it, Mankiw and Reis generalize the Lucas (1972) Phillips curve. For Lucas, roughly, output is expounded to sudden inflation[pi_t = E_{t-1}pi_t + kappa x_t.] Corporations do not see everybody else’s costs within the interval. Thus, when a agency sees an sudden rise in costs, it does not know if it’s a increased relative value or a better basic value degree; the agency expands output primarily based on how a lot it thinks the occasion is likely to be a relative value enhance. I really like this mannequin for a lot of causes, however one, which appears to have fallen by the wayside, is that it explicitly founds the Phillips curve in corporations’ confusion about relative costs vs. the value degree, and thus faces as much as the issue why ought to an increase within the value degree have any actual results.

Mankiw and Reis mainly suppose that corporations discover out the overall value degree with lags, so output depends upon inflation relative to a distributed lag of its expectations. It is clearest for the value degree (p. 1300)[p_t = lambdasum_{j=0}^infty (1-lambda)^j E_{t-j}(p_t + alpha x_t).] The inflation expression is [pi_t = frac{alpha lambda}{1-lambda}x_t + lambda sum_{j=0}^infty (1-lambda)^j E_{t-1-j}(pi_t + alpha Delta x_t).](A few of the complication is that you really want it to be (pi_t = sum_{j=0}^infty E_{t-1-j}pi_t + kappa x_t), however output does not enter that method.)

This appears completely pure and smart to me. What’s a “interval” anyway? It is sensible that corporations study heterogeneously whether or not a value enhance is relative or value degree. And it clearly solves the central persistence downside with the Lucas (1972) mannequin, that it solely produces a one-period output motion. Effectively, what’s a interval anyway? (Mankiw and Reis do not promote it this manner, and really do not cite Lucas in any respect. Curious.)

It is not instantly apparent that this curve solves the Ball puzzle and the declining inflation puzzle, and certainly one should put it in a full mannequin to take action. Mankiw and Reis (2002) combine it with (m_t + v = p_t + x_t) and make some stylized evaluation, however do not present the way to put the thought in fashions comparable to I began with or make a plot.

Their much less well-known comply with on paper Sticky Info in Common Equilibrium (2007) is a lot better for this function as a result of they do present you the way to put the thought in an specific new-Keynesian mannequin, just like the one I began with. Additionally they add a Taylor rule, and an rate of interest moderately than cash provide instrument, together with wage stickiness and some different components,. They present the way to resolve the mannequin overcoming the issue that there are lots of lagged expectations as state variables. However right here is the response to the financial coverage shock:

|

| Response to a Financial Coverage Shock, Mankiw and Reis (2007). |

Sadly they do not report how rates of interest reply to the shock. I presume rates of interest went down briefly.

Look: the inflation and output hole plots are about the identical. Apart from the slight delay going up, these are precisely the responses of the usual NK mannequin. When output is excessive, inflation is excessive and declining. The entire level was to supply a mannequin wherein excessive output degree would correspond to rising inflation. Relative to the primary graph, the primary enchancment is only a slight hump form in each inflation and output responses.

Describing the identical mannequin in “Pervasive Stickiness” (2006), Mankiw and Reis describe the desideratum nicely:

The Acceleration Phenomenon….inflation tends to rise when the economic system is booming and falls when financial exercise is depressed. That is the central perception of the empirical literature on the Phillips curve. One easy approach to illustrate this reality is to correlate the change in inflation, (pi_{t+2}-pi_{t-2}) with [the level of] output, (y_t), detrended with the HP filter. In U.S. quarterly information from 1954-Q3 to 2005-Q3, the correlation is 0.47. That’s, the change in inflation is procyclical.

Now look once more on the graph. So far as I can see, it isn’t there. Is that this model of sticky inflation a bust, for this function?

I nonetheless assume it is a neat concept price extra exploration. However I believed so 20 years in the past too. Mankiw and Reis have loads of citations however no one adopted them. Why not? I believe it is a part of a basic sample that a number of nice micro sticky value papers will not be used as a result of they do not produce a straightforward combination Phillips curve. In order for you cites, be sure that folks can plug it in to Dynare. Mankiw and Reis’ curve is fairly easy, however you continue to must maintain all previous expectations round as a state variable. There could also be other ways of doing that with trendy computational expertise, placing it in a Markov atmosphere or reducing off the lags, everybody learns the value degree after 5 years. Hank fashions have even larger state areas!

Some extra fashions

What about throughout the Fed? Chung, Kiley, and Laforte 2010, “Documentation of the Estimated, Dynamic, Optimization-based (EDO) Mannequin of the U.S. Financial system: 2010 Model” is one such mannequin. (Because of Ben Moll, in a lecture slide titled “Results of rate of interest hike in U.S. Fed’s personal New Keynesian mannequin”) They describe it as

This paper supplies documentation for a large-scale estimated DSGE mannequin of the U.S. economic system – the Federal Reserve Board’s Estimated, Dynamic, Optimization- primarily based (FRB/EDO) mannequin challenge. The mannequin can be utilized to deal with a variety of sensible coverage questions on a routine foundation.

Listed below are the central plots for our function: The response of rates of interest and inflation to a financial coverage shock.

No lengthy and variable lags right here. Simply as within the easy mannequin, inflation jumps down on the day of the shock after which reverts. As with Mankiw and Reis, there’s a tiny hump form, however that is it. That is nothing just like the Romer and Romer plot.

I will reiterate the primary level. So far as I can inform, there is no such thing as a easy financial mannequin that produces the usual perception.

Now, possibly perception is true and fashions simply must catch up. It’s attention-grabbing that there’s so little effort happening to do that. As above, the huge outpouring of new-Keynesian modeling has been so as to add much more components. Partly, once more, that is the pure pressures of journal publication. However I feel it is also an sincere feeling that after Christiano Eichenbaun and Evans, it is a solved downside and including different components is all there’s to do.

So a part of the purpose of this submit (and “Expectations and the neutrality of rates of interest”) is to argue that that is not a solved downside, and that eradicating components to search out the only financial mannequin that may produce customary beliefs is a very vital job. Then, does the mannequin incorporate something at all the customary instinct, or is it primarily based on some completely different mechanism al collectively? These are first order vital and unresolved questions!

However for my lay readers, right here is so far as I do know the place we’re. Should you, just like the Fed, maintain to plain beliefs that increased rates of interest decrease future output and inflation with lengthy and variable lags, know there is no such thing as a easy financial concept behind that perception, and definitely the usual story isn’t how financial fashions of the final 4 a long time work.