Final week, I discussed the quarterly convention calls I do for purchasers of RWM, which led to a broad dialogue of Sentiment. I need to briefly talk about the fiscal regime change desk I created for that decision (above).

The TLDR: For the previous few a long time, the US’ financial coverage has been one primarily pushed by ultra-low charges. Starting underneath Alan Greenspan, persevering with by the phrases of Ben Bernanke, Janet Yellen and now Jay Powell, low charges dominated every little thing round me. It was the alternative of CREAM.

There’s a longer dialogue available on how Zero Curiosity Price Coverage (ZIRP) impacted property priced in {dollars} or credit score, wealth inequality, and the rise of populism.1 The underside line is the primarily financial (not fiscal) stimulus responses to calamities such because the September 11th terror assaults, or the Nice Monetary Disaster had unanticipated penalties.

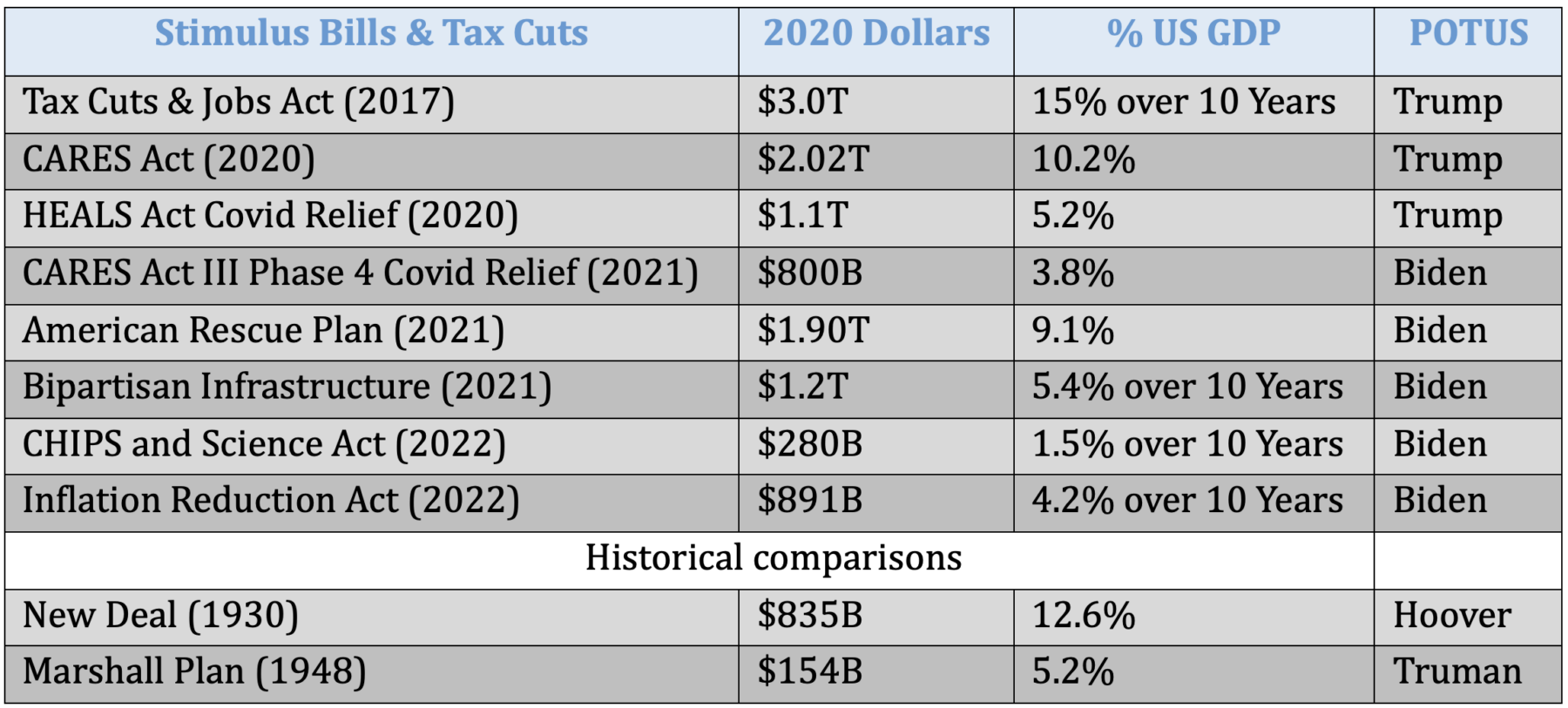

That started to vary underneath President Trump. The Tax Cuts & Jobs Act of 2017 (TCJA) was ~$three trillion unfold out throughout a decade. It was the largest fiscal stimulus to return alongside for a while, and whereas it was biased in the direction of the higher quarter of the financial strata, it was not considered broadly in the best way we usually contemplate fiscal stimulus.

Lacking its fiscal element was a big financial misunderstanding.

Then got here Covid-19. The CARES Act 1 (2020) at ~10% of GDP, was the most important fiscal stimulus for the reason that Nice Melancholy. It was adopted by the 2nd CARES Act, which added practically one other trillion {dollars} of stimulus. The three of those had an enormous stimulatory affect.

Then President Biden got here into workplace; he handed the third CARES Act, the American Rescue Plan, the Bipartisan Infrastructure Invoice, the Chips Act, and the Inflation Discount Act. (Knowledge within the desk are totals, however practically half of these allocations have been new cash 2). Regardless it was one other trillion and a half {dollars} in quick stimulus and some trillion {dollars} extra unfold out over 10 years.

On the similar time, federal funds charges went from zero to over 5%. The affect on shares and bonds was unmistakable.

The 2010s have been a decade of financial stimulus that noticed fairness markets acquire 14% yearly. Free cash! At the least, low-cost capital, low-cost financing for shopper and business purchases, all of which led to greater company earnings.

It’s very cheap to presume that dearer cash means greater prices of financing these shopper and business purchases; it will in all probability crimp whole retail gross sales, and will negatively affect company earnings (finally).

Therefore, you must decrease your expectations for future fairness positive aspects within the period following ZIRP and QE. If we have been getting 12-14% beforehand, then the 2020s ought to anticipate one thing nearer to 5-7% in fairness returns.

However concurrent with that’s the fastened earnings portion of your portfolios. I’ll spend extra time in a future put up detailing why “Money is not trash,” however the backside line is way of what you lose on the fairness aspect, you acquire on the fastened earnings aspect. This bodes properly for these searching for earnings, who make investments through a 60/40 portfolio, or are in any other case lower-risk traders.

Most of what takes place within the day-to-day world of markets is noisy and meaningless; however the shift from financial to fiscal stimulus may be very, very important.

Traders would do properly in listening to this regime change.

Beforehand:

The Biggest Missed Alternative of Our Lifetimes (October 23, 2023)

What Else Is perhaps Driving Sentiment? (October 19, 2023)

Farewell, TINA (September 28, 2022)

__________

1. We are going to save that for an additional put up…

2. I defined throughout the name that a lot of these {dollars} had been already allotted in different payments and have been consolidated underneath every of those items of laws. Regardless, it was nonetheless trillions in fiscal stimulus.