Everyone is ready with bated breath for immediately’s 2:00 announcement in regards to the charges, however let me spare you the suspense:

They’re completed with fee hikes this cycle. The following change in charges is extra more likely to be down than up.

At the least, if Powell & Firm actually had a deal with on what has been driving inflation for the previous few years, that might be their place.

It has been irritating watching the FOMC come round to finally making the best resolution, however all too usually, they’re late to the get together: Late getting off of emergency footing, late to start elevating charges in response to surging inflation in 2021, late to see this was being pushed by fiscal not financial stimulus of the pandemic, late to acknowledge the FOMC itself is a driver of housing inflation, and eventually, late to acknowledge inflation had peaked and reversed.

I’m not certain in the event that they fairly acknowledge the potential injury they’re doing to the economic system. I don’t see any indication the FOMC understands that shortages in single-family houses, rental items, semiconductors, vehicles, and Labor received’t be cured by greater charges. In lots of instances, they’ll solely be exacerbated.

That’s very true in housing, the place the Fed is creating new issues and making current ones even worse:

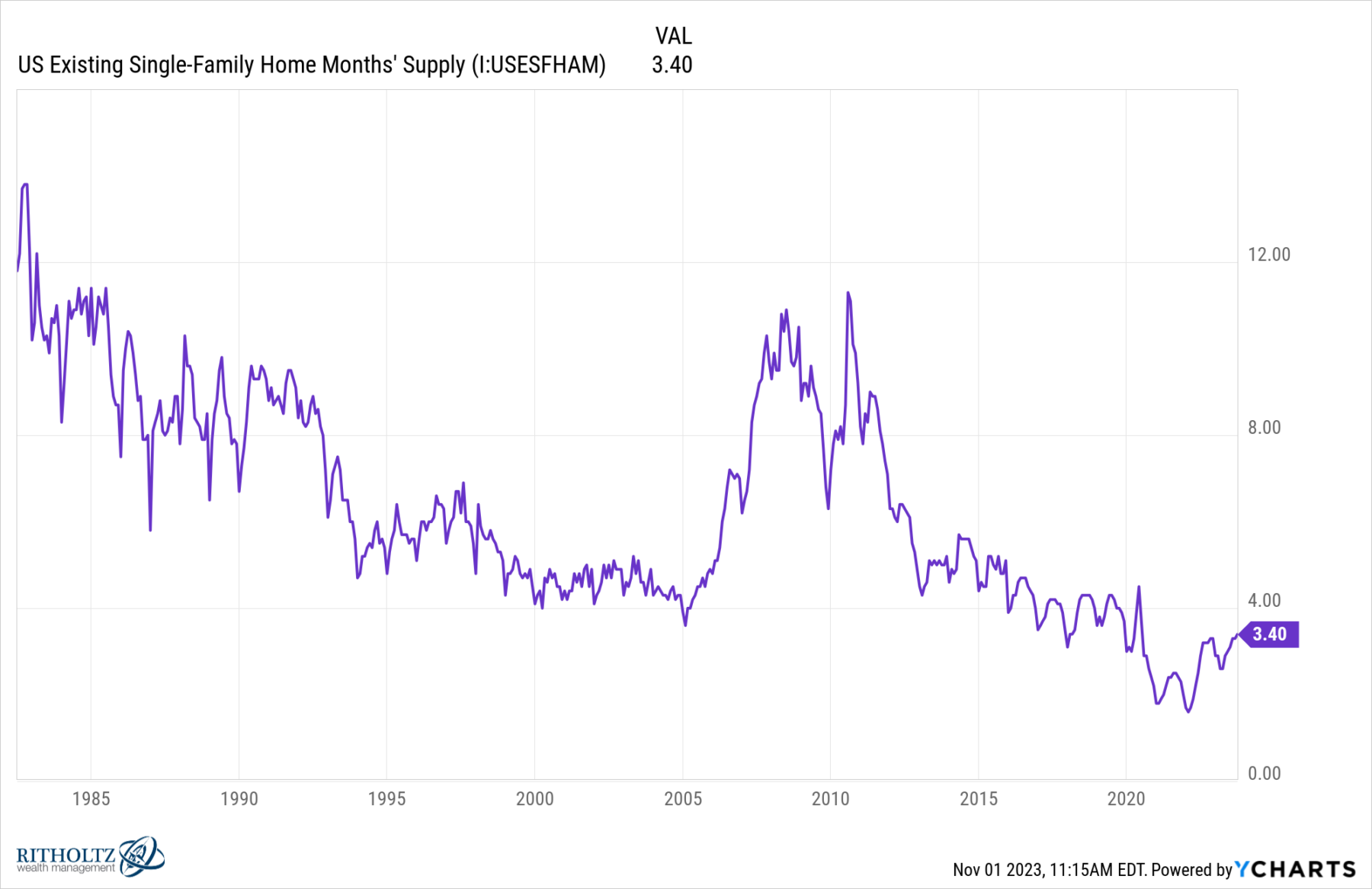

1. Lack of Single Household Houses: We’ve mentioned this earlier than most notably in 2021, however house builders have wildly underbuilt the variety of homes relative to inhabitants progress following the monetary disaster (GFC). That’s 15 years of under-building houses following 5 years of overbuilding them. In the meantime, the US inhabitants continues to develop and family formation has ticked up dramatically following the pandemic.

Because the chart above exhibits, we’re off the lows of 2022, however apart from through the pandemic, the Months’ Provide of current houses on the market is at its lowest stage going again 40 years.

There is just too little provide relative to not simply demand however want.

2. Low Mortgage Charge Golden handcuffs: Roughly 60% of householders with a mortgage have charges of 4% or decrease. This prevents individuals from shifting to a brand new house, no matter whether or not they’re shifting up or downsizing. Charges between 7 and eight% merely make the month-to-month carrying prices too dear; that is true whatever the buy value.

If the Fed needs to see housing costs average, an appointment leases fall, we want a a lot larger provide of single-family houses. I don’t know why it’s so counterintuitive to see that occurs with decrease mortgage charges. The FOMC clearly mustn’t return to zero however someplace within the low 4s% is a significantly better fed funds fee than the place we’re immediately. It shouldn’t take a recession to get there.

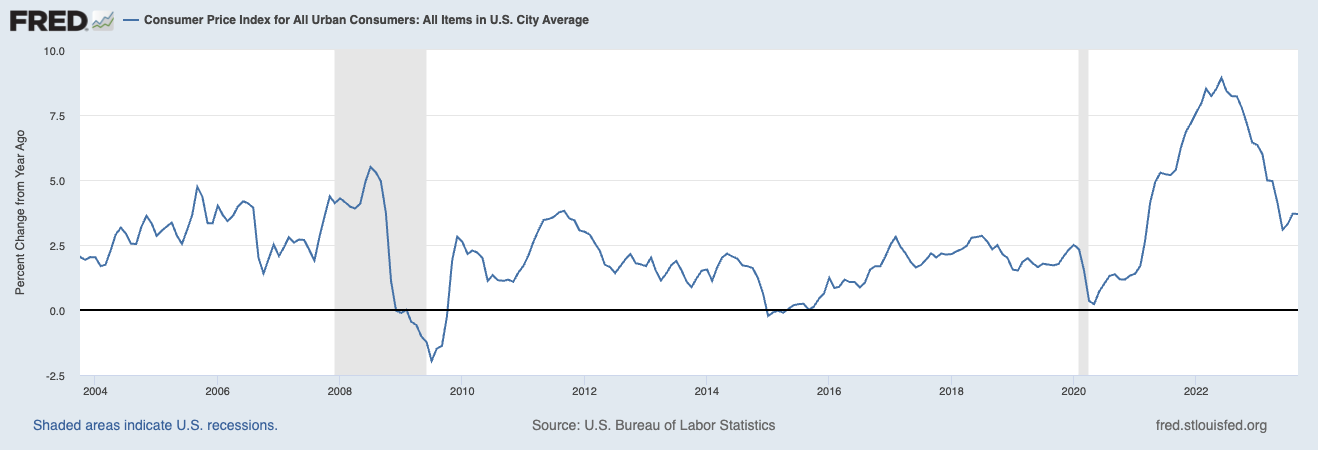

3. Proprietor’s Equal Hire: It lags badly versus different measures of rental value adjustments. (this is the reason I believe the Fed believes inflation is worse than it’s).

It is usually price noting that through the GFC, Homeowners’ Equal Hire understated inflation period when so many individuals we’re capable of make the most of low charges and no credit score requirements to pile into house purchases; immediately the shortage of provide and elevated charges has OER overstating rental inflation.

Exterior of housing, it’s fairly clear that labor and vehicles are the opposite sources of elevated costs that financial coverage isn’t reaching. Selective meals shortages are problematic; wars within the Center East and Ukraine are additionally making oil pricier, and The Fed has no management over these geopolitical occasions through fee will increase.

As famous over the summer time, The Fed is on the verge of snatching defeat from the jaws of victory. Let’s hope they determine this out sooner somewhat than later.

~~~

You’ll be able to see Powell’s presser immediately at 2:30.

Beforehand:

5 Methods the Fed’s Deflation Playbook May Be Improved (Businessweek, August 18, 2023)

For Decrease Inflation, Cease Elevating Charges (January 18, 2023)

Inflation Comes Down Regardless of the Fed (January 12, 2023)

Who Is to Blame for Inflation, 1-15 (June 28, 2022)

Why Is the Fed At all times Late to the Get together? (October 7, 2022)

Understanding Investing Regime Change (October 25, 2023)

__________

* …Elevating Charges

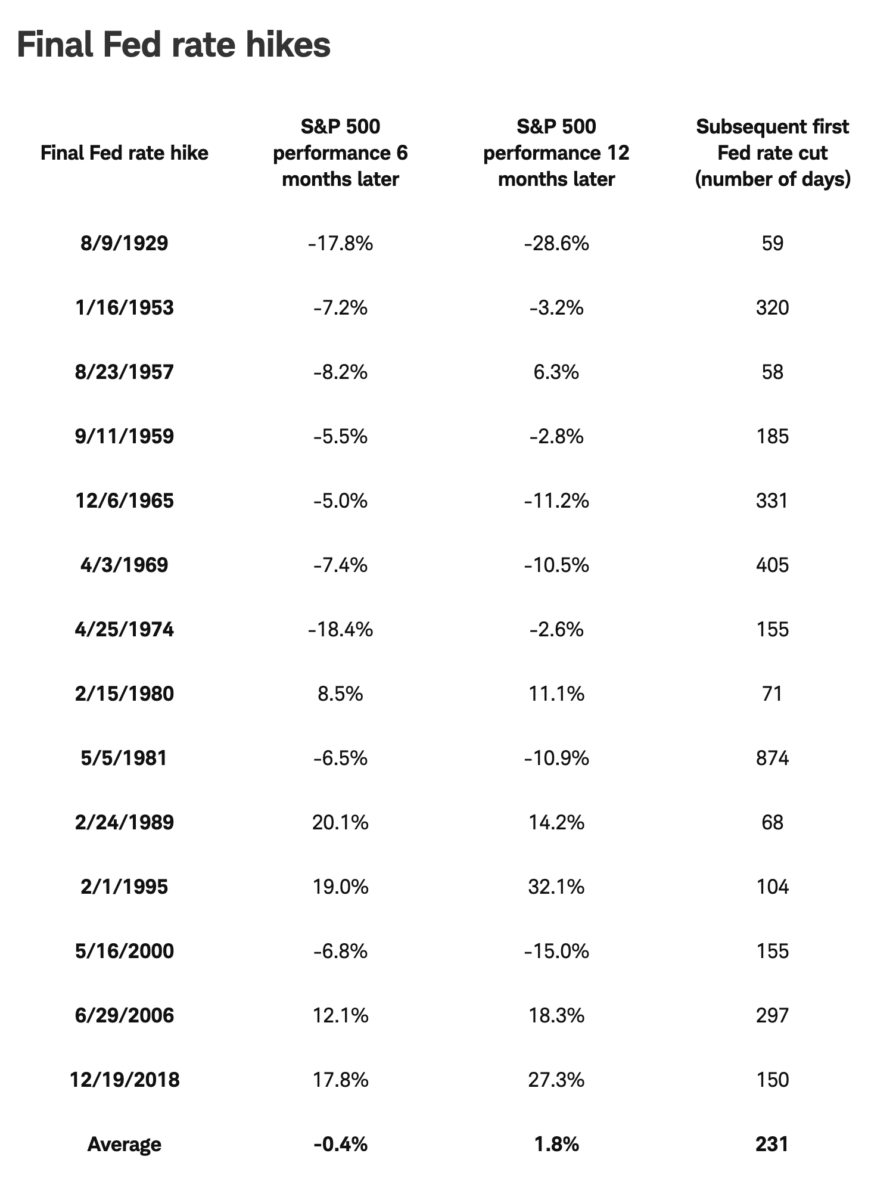

Through Liz Ann Sonders:

Nothing Typical for Shares After Fed’s Final Hike

Supply: Schwab