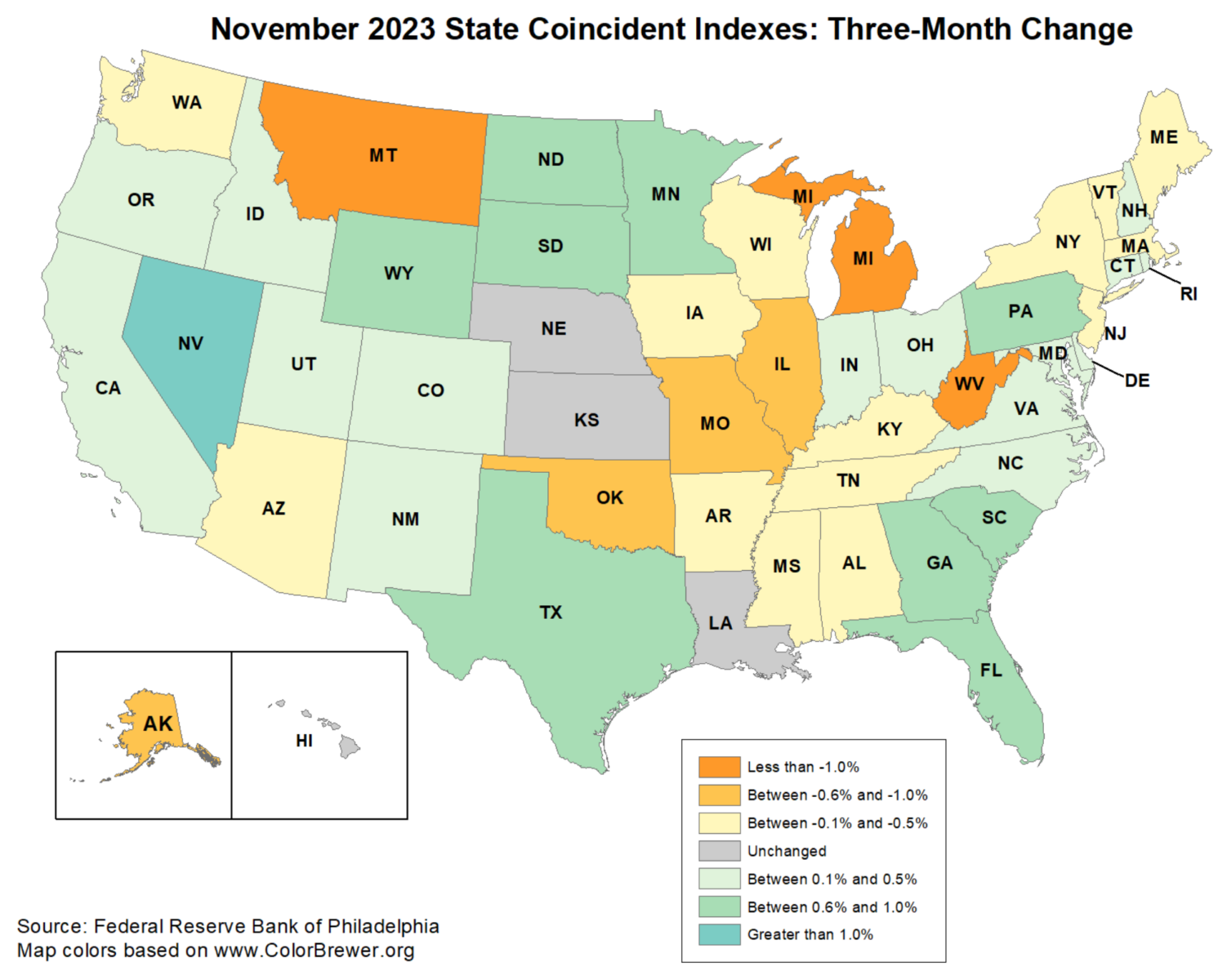

I’m coming out of ebook go away to share this single knowledge level that snuck out over the vacations: The Federal Reserve Financial institution of Philadelphia’s State Coincident Indicators for November 2023.

I just like the SCI – its broad, constant, and doesn’t function with too massive of a lag.

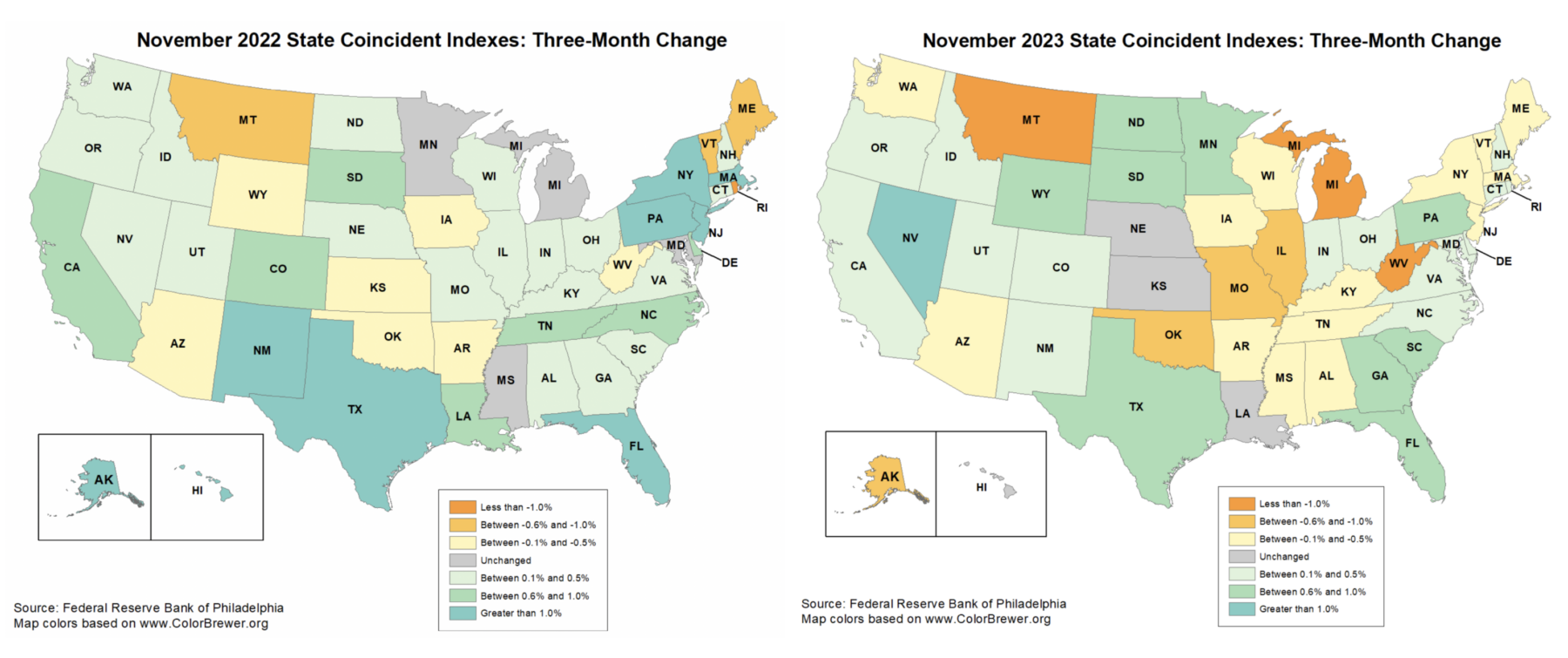

Over the previous three months, the indexes elevated in 25 states, decreased in 21 states, and remained steady in 4, for a three-month diffusion index of 8. Evaluate this with the identical interval one 12 months in the past, when the coincident indexes elevated in 30 states, decreased in 13 states, and remained steady in seven, for a one-month diffusion index of 34.

To tremendously over-simplify the SCI: Eight extra states at the moment are contracting now (extra orange/yellow) versus a 12 months in the past; 5 fewer states are increasing at present (much less blue/inexperienced) than similar Three month interval in 2022:

State Coincident Indicators 1 Yr In the past versus In the present day

I watch this to see how shut we’re to falling right into a recession, and to get an concept of when the FOMC shall be compelled to acknowledge the influence of their open market rate of interest handiwork.

It is a modest change, and certain not sufficient to push the Fed to behave instantly. But when it will get a lot worse, it might pressure their hand. If this continues to decelerate, the FOMC is likely to be slicing charges within the first half of the 12 months. If November was a blip, and we see extra enlargement and fewer contraction, then it’s the again half of the 12 months or later.

I’ll maintain monitoring this every month…

Supply:

State Coincident Indexes: Launch

The Federal Reserve Financial institution of Philadelphia, December 29, 2023

Beforehand:

State Coincident Indicators: November 2022 (January 4, 2023)

Indicators of Softening (July 29, 2022)

Why Recessions Matter to Buyers (July 11, 2022)

__________

1: The State Coincident Indicators are composed of 4 state-level variables: 1) Nonfarm payroll employment; 2) Common hours labored in manufacturing by manufacturing staff; 3) Unemployment fee; and 4) Wage and wage disbursements deflated by the patron value index.