Economics is about fixing a number of little puzzles. At a July 4th celebration, an excellent sensible pal — not a macroeconomist — posed a puzzle I ought to have understood way back, prompting me to know my very own fashions a little bit higher.

How will we get inflation from the large fiscal stimulus of 2020-2021, he requested? Properly, I reply, individuals get lots of authorities debt and cash, which they do not assume shall be paid again through increased future taxes or decrease future spending. They know inflation or default will occur eventually, in order that they attempt to do away with the debt now whereas they will quite than put it aside. However all we are able to do collectively is to attempt to purchase issues, sending up the value stage, till the debt is devalued to what we count on the federal government can and can pay.

OK, requested my pal, however that ought to ship rates of interest up, bond costs down, no? And rates of interest stayed low all through, till the Fed began elevating them. I mumbled some excuse about rates of interest by no means being superb at forecasting inflation, or one thing about danger premiums, however that is clearly unsatisfactory.

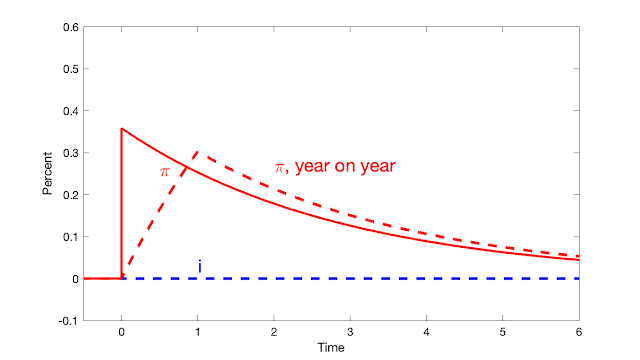

In fact, the reply is that rates of interest don’t want to maneuver. The Fed controls the nominal rate of interest. If the Fed retains the brief time period nominal rate of interest fixed, then nominal yields of all bonds keep the identical, whereas fiscal inflation washes away the worth of debt. I ought to have remembered my very own central graph:

That is the response of the usual sticky value mannequin to a fiscal shock — a 1% deficit that’s not repaid by future surpluses — whereas the Fed retains rates of interest fixed. The strong line is instantaneous inflation, whereas the dashed line provides inflation measured as % change from a yr in the past, which is the frequent option to measure it within the information.